Why Standard Carriers Reject DUI-Plus-Accident Applications

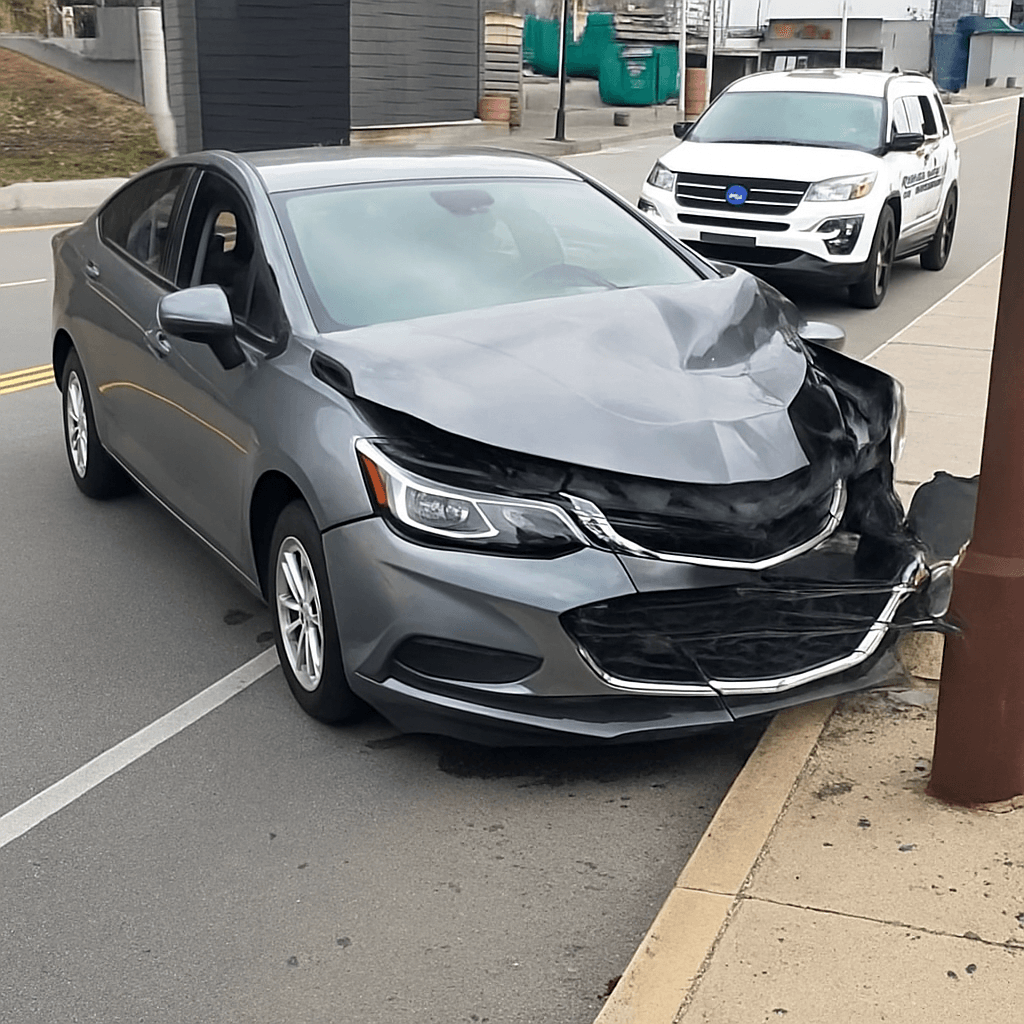

You received a DUI conviction, then had an at-fault accident while your case was pending or shortly after reinstatement. Colorado DMV requires SR-22 insurance to reinstate your license, but when you request quotes online, every major carrier either rejects your application outright or returns error messages. The rejection is not about the SR-22 filing — Progressive, GEICO, State Farm, and others all file SR-22 in Colorado. The rejection is about underwriting risk tier.

Standard and preferred carriers use automated underwriting systems that assign risk scores based on violation history. A single DUI moves most drivers to the non-standard tier. An at-fault accident within three years of a DUI crosses the threshold where standard carriers cannot profitably write the policy under their rating structures. The system flags the dual trigger and routes your application to non-standard specialists or rejects it entirely. This is not a coverage availability problem — it is a tier assignment problem.

Compare car insurance rates in your state

Get quotes from licensed carriers — no obligation, no spam, results in minutes.

Get Your Free QuoteColorado SR-22 Filing Period

3 years

Colorado requires continuous SR-22 filing for 3 years following DUI conviction. Any lapse in coverage during this period triggers an automatic suspension and restarts the 3-year clock from the date you refile.

Colorado Division of Motor Vehicles reinstatement requirements

What Non-Standard Tier Actually Means for Your Situation

Non-standard auto insurance is not a separate product — it is the same liability, collision, and comprehensive coverage written under a different risk pool and rating structure. Carriers that specialize in non-standard underwriting accept drivers with multiple violations, license suspensions, and layered risk factors that standard carriers reject. The coverage itself meets Colorado's minimum liability requirements and satisfies SR-22 filing obligations identically to a standard policy.

The structural difference is premium calculation. Non-standard carriers use rating factors that account for dual-trigger scenarios without automatic rejection. Where a standard carrier might apply a 150% surcharge for DUI and then reject the application entirely when adding the accident, a non-standard specialist prices both violations into the base premium from the start. The result is a higher monthly cost, but the application is approved and the SR-22 is filed.

Colorado's minimum liability limits are $25,000 per person for bodily injury, $50,000 per accident for bodily injury, and $15,000 for property damage. Non-standard carriers in Colorado frequently write policies at exactly these minimums to keep premiums manageable for drivers in your situation. You are not required to carry collision or comprehensive coverage unless you have a loan or lease requiring it.

The blocker is not finding SR-22 coverage — it is finding a carrier whose underwriting system will approve a policy with both a DUI and a recent at-fault accident on the same application.

Carriers Writing DUI-Plus-Accident Policies in Colorado

Non-standard specialists (Bristol West, Dairyland, The General, Infinity, National General) underwrite high-risk drivers as their primary business. These carriers accept DUI-plus-accident applications without manual review in most cases, offer online quotes or broker-assisted quotes within 24 hours, and file SR-22 electronically to Colorado DMV immediately upon policy binding. Monthly premiums for minimum liability coverage typically fall between $180 and $320 depending on age, county, and the accident's severity. Bristol West and Dairyland both operate statewide in Colorado and write non-owner SR-22 policies for drivers without a vehicle.

Standard carriers with non-standard divisions (Progressive, GEICO) sometimes approve dual-trigger applications if the accident was minor (under $5,000 in damages) and the DUI conviction is more than 18 months old. These approvals are not guaranteed and often require a phone call to an underwriter rather than an instant online quote. If approved, the premium sits between standard and true non-standard rates. State Farm writes SR-22 in Colorado but typically declines applications with both a DUI and an accident unless both are older than 24 months.

Related Articles

How the Accident's Fault Status and Timing Affect Approval

Colorado is an at-fault state, meaning the driver responsible for causing the accident is liable for damages. If you were cited for the accident or your insurance paid the claim, underwriting systems treat it as an at-fault accident regardless of whether the other driver also received a citation. Not-at-fault accidents (where the other driver was cited and their carrier paid) do not trigger the dual-violation underwriting block in most cases, though they still appear on your driving record.

Timing matters because underwriting systems weight recent violations more heavily. An accident that occurred within six months of your DUI conviction signals ongoing risk and narrows carrier availability significantly. If the accident occurred 18 to 24 months after the DUI, some standard carriers with non-standard divisions will consider the application. Accidents older than 36 months typically fall off the active surcharge window, though they remain visible on your Motor Vehicle Report for longer.

If the accident occurred while you were driving on a restricted license or during your DUI suspension period, expect automatic rejection from all standard carriers and prepare for manual underwriting review even with non-standard specialists. Driving under suspension is a separate violation that compounds the dual-trigger scenario into a triple-trigger one.

Colorado License Reinstatement Fee

$95

After completing your suspension period and DUI requirements (Level II Alcohol Education, ignition interlock if applicable, court fines), you pay a $95 reinstatement fee to Colorado DMV. This fee is separate from SR-22 filing fees and insurance premiums.

Colorado Division of Motor Vehicles reinstatement fee schedule

Non-Owner SR-22 as the Path If You Sold Your Vehicle

If you no longer own a vehicle — whether you sold it after the DUI, lost it in the accident, or cannot afford to insure it at non-standard rates — Colorado allows non-owner SR-22 policies to satisfy reinstatement requirements. A non-owner policy provides liability coverage when you drive a vehicle you do not own: a borrowed car, a rental, or a vehicle provided by an employer. It does not cover a vehicle registered in your name.

Non-owner SR-22 premiums are substantially lower than standard policies because the carrier assumes you drive infrequently. For a DUI-plus-accident scenario in Colorado, non-owner policies from Dairyland, The General, or GEICO typically cost $60 to $110 per month for state minimum liability limits. The SR-22 filing fee (usually $15 to $25, set by the carrier) is the same whether you buy a standard or non-owner policy. The non-owner policy satisfies Colorado's continuous insurance requirement during your 3-year SR-22 period even if you do not currently drive.

What Happens Next: Filing, Reinstatement, and the Ignition Interlock Requirement

Once you bind a policy with a carrier that writes your dual-trigger scenario, the carrier files the SR-22 certificate electronically with Colorado DMV within one business day. You do not file the SR-22 yourself — the insurance company is the filing entity. Colorado DMV updates your record to show proof of financial responsibility, which clears the insurance requirement for reinstatement. You still must complete all other DUI reinstatement requirements: Level II Alcohol Education, ignition interlock device installation (required for all DUI convictions in Colorado), payment of court fines, and the $95 reinstatement fee.

Colorado requires ignition interlock devices for a minimum of 8 months for first-offense DUI, 2 years for second offense, and longer for subsequent offenses or high BAC cases. The IID requirement runs concurrently with your SR-22 requirement, not sequentially. Your SR-22 policy must remain active for the full 3-year period even after your IID requirement ends. If your policy lapses or cancels for non-payment during the 3-year SR-22 window, Colorado DMV suspends your license again immediately and restarts the 3-year clock when you refile. The carrier is required to notify DMV of any cancellation or lapse within 10 days.

Start with Non-Standard Specialists and Work from Confirmed Availability

Request quotes from Bristol West, Dairyland, The General, and Infinity first — these carriers underwrite DUI-plus-accident scenarios as standard business and approve applications that other carriers reject automatically. If you still own a vehicle, provide the VIN, your current address, and your Colorado driver's license number when requesting the quote. If you no longer own a vehicle, specify that you need a non-owner SR-22 policy. Most non-standard specialists offer online quote tools, but dual-trigger cases often require a phone call to complete underwriting. Expect the quote process to take 24 to 48 hours if manual review is needed.

After binding the policy, confirm with the carrier that the SR-22 has been filed electronically and request a copy of the filing confirmation for your records. Colorado DMV does not send you a confirmation when they receive the SR-22 — the carrier's filing confirmation is your proof. Once the SR-22 is on file and you have completed all other reinstatement requirements, schedule your reinstatement appointment with Colorado DMV. Bring proof of ignition interlock installation, your Level II Alcohol Education completion certificate, proof of payment for all court fines, and the $95 reinstatement fee. Compare non-standard carriers writing your situation now.